Quantitative ALM & Market Risk Modeler - Treasury Capital Markets

Lone Tree, Colorado; Westlake, Texas; New York, New York; Chicago, Illinois

Requisition ID 2024-98775 Category Risk & Regulatory Position type Regular Salary USD $87,800 - $195,200 / Year Application deadline 2024-07-29Your opportunity

At Schwab, you’re empowered to make an impact on your career. Here, innovative thought meets creative problem solving, helping us “challenge the status quo” and transform the finance industry together.

The Treasury Capital Markets (TCM) function within Corporate Treasury manages fixed-income investments in several portfolios totaling approximately $500 billion in balance sheet assets and approximately $100 billion in off-balance-sheet brokered deposit agreement notional investments primarily for the benefit of the Charles Schwab Corporation and its banking and broker-dealer subsidiaries. The Asset Liability Management (ALM) team within TCM is responsible for balance sheet management strategy, portfolio and brokered deposit notional investment allocation decisions, balance sheet modeling and analytics, market risk management, ALM derivatives, and net interest revenue forecasting.

As an individual contributor within the ALM team focused on Market Risk Modeling, you will play a key role in the overall interest rate risk management, strategic optimization of the balance sheet, and corresponding NIM profile through the development and execution of a robust market risk modeling framework in collaboration with business partners, including investment portfolio managers, risk partners, and product leaders across the firm.

In this role, you will be responsible for modeling, analytics, attribution, and automation for all market risk management related to all on-balance-sheet and off-balance-sheet exposures, including fixed-income investment portfolios, off-balance sheet brokered deposit notional investments, interest rate derivatives, and income modeling associated with all remaining components of the balance sheet. This individual will work closely with the ALM Analytics team and ALM Strategy team to optimize our ALM and Market Risk positioning and support allocation decisions and strategy.

What you have

- Three years relevant experience or combination of time in post graduate studies.

- Degree in a quantitative field such as Applied Mathematics, Engineering, or Economics is required. CFA, FRM, or PRM designations a plus.

- Strong quantitative skills in fixed income investment modeling and analytics

- Strong knowledge of fixed income modeling in systems such as PolyPaths, BlackRock, Murex, Intex, Bloomberg, QRM, Calypso, etc. is highly preferred.

- Expertise in balance sheet modeling, net interest revenue modeling, and/or EVE modeling

- Direct experience in modeling derivatives and associated hedge accounting

- Experience with Python and SQL or another general-purpose programming language is strongly preferred.

- Experience working with an enterprise risk analytics system with automation features such as PolyPaths Enterprise is desired.

- Knowledge of premium discount amortization and associated impact of principal prepayments on NII

- Knowledge of securities accounting standards and implementation

- Enthusiasm to work in white space and the ability to create innovative analyses to help drive the strategy and risk management of the balance sheet

- Ability to multi-task while maintaining composure in a potentially fast-paced environment

- Strong written and oral communication skills

What you'll do:

- Perform front-office modeling, analytics, and optimization focusing on Market Risk Management with expert knowledge of fixed-income, derivatives, and balance sheet modeling.

- Develop a robust Market Risk Management modeling framework focusing on Economic Value of Equity (EVE) sensitivity, Capital at Risk, Net Interest Income (NII) sensitivity, and other industry standard metrics.

- Contribute to initiatives to enhance, streamline, and automate balance sheet analytics, NII forecast, and dynamic NII sensitivity measurement.

- Play a key role in achieving risk-return optimization mandate within ALM subject to external/macro-economic factors as well as a strong market risk management framework.

- Support ALM Strategy, ALM Analytics, and Investments teams via new and existing capabilities, tools, reports, attributions, and optimizations to inform the optimal positioning of the investment portfolio through rate cycles, with a significant emphasis on risk management.

- Collaborate with key business partners to drive balance sheet analytics to support investment allocation decisions, strategy, and risk management.

- Leverage industry investment research and stay abreast of peer and industry trends.

In addition to the salary range, this position is also eligible for bonus or incentive opportunities

What’s in it for you

At Schwab, we’re committed to empowering our employees’ personal and professional success. Our purpose-driven, supportive culture, and focus on your development means you’ll get the tools you need to make a positive difference in the finance industry. Our Hybrid Work and Flexibility approach balances our ongoing commitment to workplace flexibility, serving our clients, and our strong belief in the value of being together in person on a regular basis.

We offer a competitive benefits package that takes care of the whole you – both today and in the future:

- 401(k) with company match and Employee stock purchase plan

- Paid time for vacation, volunteering, and 28-day sabbatical after every 5 years of service for eligible positions

- Paid parental leave and family building benefits

- Tuition reimbursement

- Health, dental, and vision insurance

Eligible Schwabbies receive

-

Medical, dental and vision benefits

-

401(k) and employee stock purchase plans

-

Tuition reimbursement to keep developing your career

-

Paid parental leave and adoption/family building benefits

-

Sabbatical leave available after five years of employment

-

March 27, 2023

March 27, 2023 -

Students We’re all-in when it comes to developing talent – from internships and academies to our tech leader program. April 12, 2023

-

Diversity and inclusion We make sure everyone feels valued, supported, and welcomed. Because that’s what moves us forward. April 12, 2023

-

Schwab stories There’s no better way to discover life at Schwab than hearing it from the amazing people who experience it every day. April 12, 2023

-

March 23, 2023

-

Schwab stories There’s no better way to discover life at Schwab than hearing it from the amazing people who experience it every day. April 13, 2023

-

April 18, 2023

-

June 29, 2023

-

June 30, 2023

-

July 03, 2023

-

July 06, 2023

-

Students We’re all-in when it comes to developing talent – from internships and academies to our tech leader program. July 07, 2023

-

July 07, 2023

-

July 10, 2023

-

June 26, 2023

-

Diversity and inclusion We make sure everyone feels valued, supported, and welcomed. Because that’s what moves us forward. June 30, 2023

-

July 03, 2023

-

Schwab Employee Benefits & Compenstation Our Total Rewards are designed to support the whole you – now, and in the future. Learn more about the benefits of working at Schwab. July 03, 2023 Benefits Home Page Related Content SR Sidebar Related Content

-

July 06, 2023

-

Schwab Stories There’s no better way to discover life at Schwab than hearing it from the amazing people who experience it every day. July 07, 2023

-

July 11, 2023

-

July 06, 2023

-

July 10, 2023

-

July 11, 2023

-

June 27, 2023

-

June 28, 2023

-

July 03, 2023

-

Client Service At Schwab, our commitment to seeing the world “through clients’ eyes” underlines everything we do, and our Client Service & Support team is often the first place client's experience it. July 07, 2023 Service Related Content

-

July 07, 2023

-

July 07, 2023

-

6 Tips for Career Success as a College Graduate: Advice from a Schwab Campus Recruiter Graduating from college is a momentous occasion and it can be hard knowing where to start after earning your degree. As you're looking for your next opportunity, make sure to check out these helpful tips and words of advice from a Schwab Campus Recruiter to set yourself up for career success! June 21, 2023 Interns & Early Careers Story Hub

-

Benefits Spotlight: Matt B.'s Adventures While on Sabbatical Read how Matt B., a V.P. Branch Manager, used Schwab's Sabbatical Benefit to explore Africa with his family. June 21, 2023 Benefits Story Hub Home Page Related Content

-

How to Become a Financial Consultant: Jordan’s Journey Through the FCA Program | Schwab Jobs Are you a recent graduate looking to pursue a purposeful & meaningful career in Finance? If so, Schwab’s Financial Consultant Academy may be the perfect place for you. Read on to see how Jordan is paving his way to becoming a Financial Consultant and the professional development opportunities he's had in this program! June 21, 2023 Life at Schwab Story Hub

-

Career Development: Les S. Builds a Diverse Career at Schwab Read how Les S. in Digital Product Management reinvented her career path to support innovation at Schwab. June 21, 2023 Career Development Story Hub

-

Women in Finance: Mayra C.'s Path to Leadership Learn how Mayra C., a VP Financial Consultant, built an impactful career as a woman in finance. June 21, 2023

-

Brandon's Commitment to Service | Schwab Jobs Discover how Brandon is transforming the lives of others through passionate customer service & volunteerism. June 21, 2023 Culture & Inclusion

-

Reach for the S.T.A.R.s: How to Prepare for a Behavioral-Based Interview at Schwab Interviewing is a necessary and essential part of the job application process. Here at Schwab, our interviewing approach stems from a behavioral-based interviewing methodology. Read on for advice and further information on the best way to prepare for an interview at Schwab! June 21, 2023 Career Development Story Hub

-

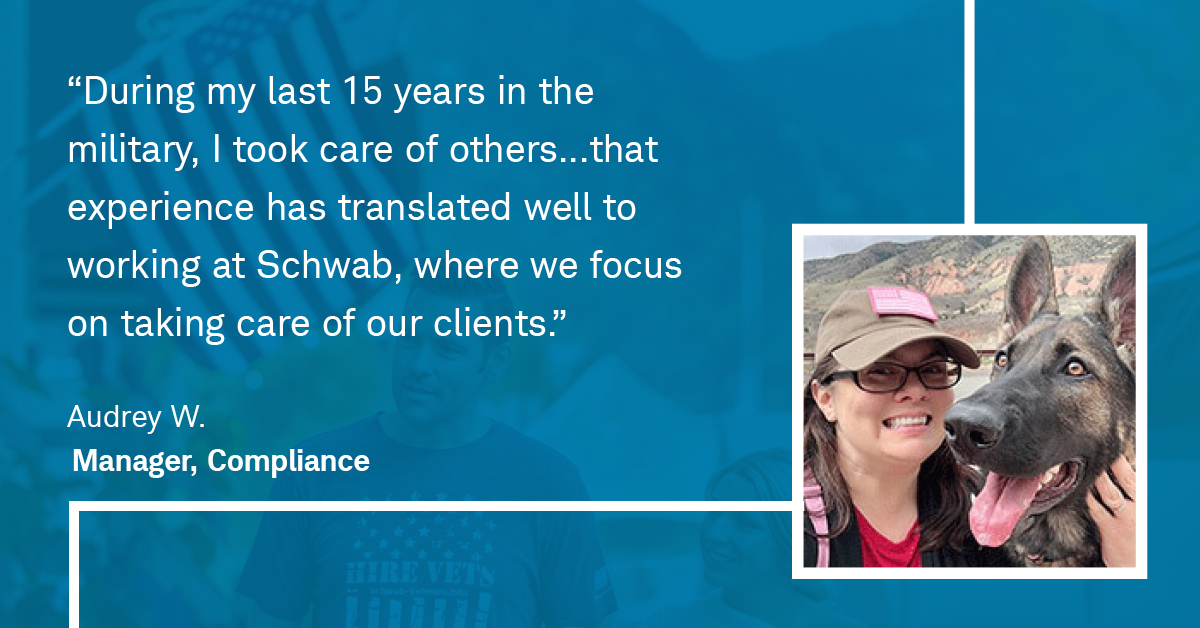

Hiring Our Heroes: Audrey, Veteran & Compliance Manager Read how Veteran Audrey W. found a Compliance Manager opportunity at Schwab through our Hiring Our Heroes partnership June 21, 2023 Culture & Inclusion Home Page Related Content

-

Building a Career at Schwab: Travis's Story Read how Travis uncovered his career opportunity and gained professional development in Wealth Management as a Financial Consultant at Charles Schwab. July 20, 2023 Career Development

-

Intern to Schwabbie, Dillon's Story Celebrating National Intern Day: Learn how Dillon went from Intern Academy to full time employee to Employee Resource Group (ERG) creator & leader. July 27, 2023 Interns & Early Careers Story Hub

-

Military Veterans Network: Tammy's Story Learn how Tammy supports veterans through our employee resource group Military Veterans Network at Schwab. July 28, 2023 Culture & Inclusion Story Hub

-

ERG Spotlight: Pride+ Happy PRIDE month! Learn about our LGBTQ+ Employee Resource Group at Schwab PRIDE+. July 31, 2023 Culture & Inclusion Story Hub

-

Veteran Finds Work-Life Balance and Community at Schwab Read how military veteran Jordan H. found work/life balance and became a leader in the Families Network at Schwab. August 01, 2023 Culture & Inclusion Story Hub

-

Jackie's FINRA Series 7 Exam Journey Read how passing the Series 7 exam transformed Jackie's career trajectory, and how the support she encountered at Schwab helped her become a Financial Consultant Partner at our firm. August 10, 2023 Career Development Story Hub Retail Related Content

-

August 16, 2023

-

Hybrid work & flexibility at Schwab. Learn about our hybrid work schedule that provides you the freedom to work from home and office. August 10, 2023

-

ERG Spotlight: Schwab Organization of Latinx (SOL) Read how our Schwab Organization of Latinx (SOL) Employee Resource Group empowers Latinx individuals to succeed in their professional careers. September 13, 2023 Culture & Inclusion Story Hub

-

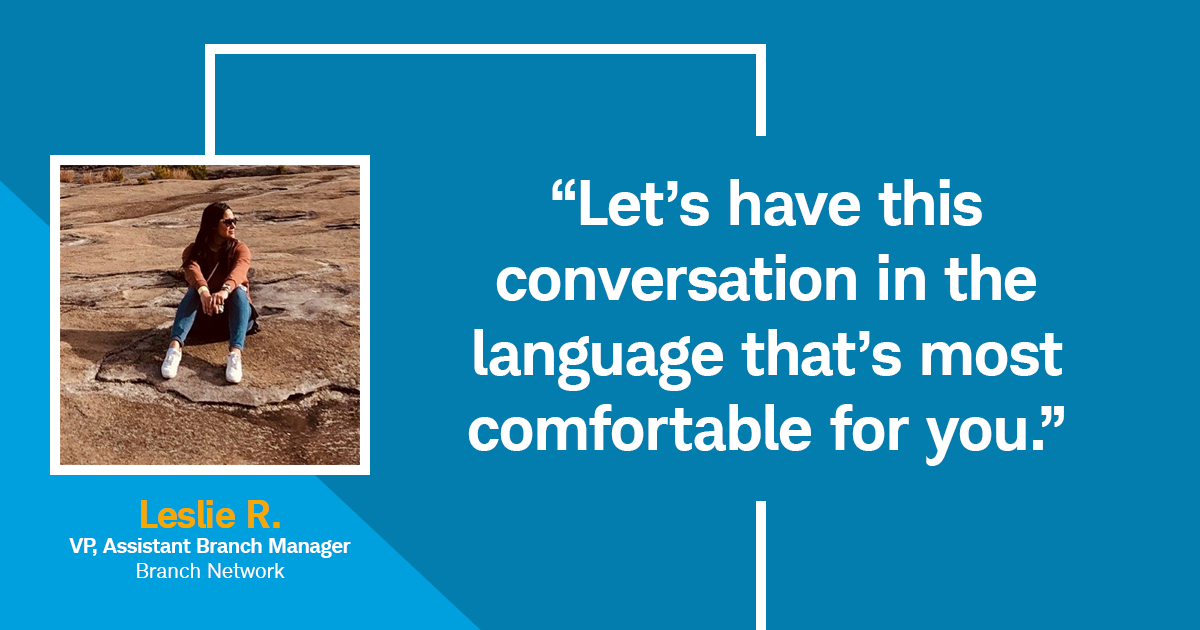

Career Development: How Leslie R. Grew Professionally & Forged Connections Through Shared Culture Read how Leslie R. experienced career development at Schwab while using her cultural background to make finance accessible to non-English speaking clients. September 21, 2023 Career Development Story Hub

-

Driving Change Through Diverse Leadership Schwabbie Doug A. was nominated by our Black Professionals at Charles Schwab (BPACS) Employee Resource Group to be a part of the IMPACT Development Program. Read how the program inspired him to “help African Americans gain access to capital…build community, and move our D&I strategy forward.” September 25, 2023 Culture & Inclusion Story Hub

-

Women in Tech: Olivia V. Meet Olivia V., one of our Technology Product Management superstars. Read how, over the course of 13 years at Schwab, she’s transitioned from finance into tech and built an impactful career. September 29, 2023 Career Development Story Hub Home Page Related Content Technology Related Content

-

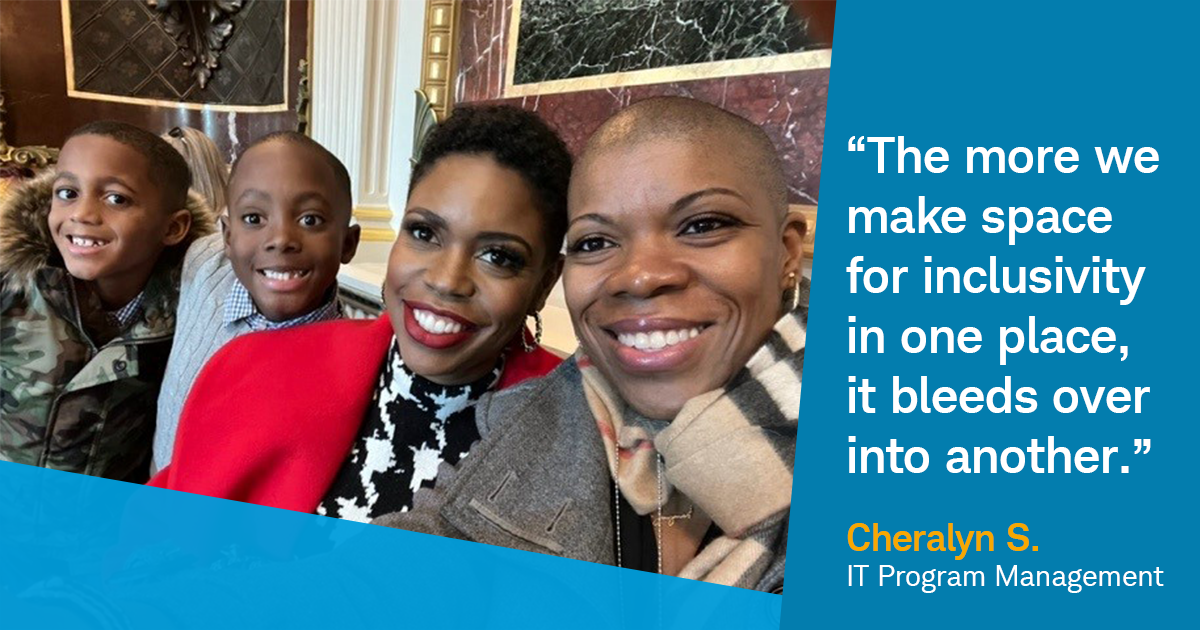

Allyship Matters: Finding Success and Authenticity at Home and at Work In recognition of National Coming Out Day, we’re highlighting Cheralyn S., a leader in IT Program Management and member of the LGBTQ+ community. Read about her coming-out journey and learn how she found allyship and authenticity in the workplace and beyond. October 11, 2023 Culture & Inclusion Story Hub

-

Build Your Career: 30 Years at Schwab with Robert K., VP Branch Manager Learn how Robert K., a 30-year Schwabbie and VP Branch Manager, used his passion for investment to experience career growth, professional stability, and become a leader in finance. October 23, 2023 Career Development Story Hub Retail Related Content

-

Career Changer: Academia to Financial Services Learn how Miranda used her degree in Machine Learning to transition from a scientific researcher to a brokerage specialist in Trader Services. November 06, 2023 Career Development Story Hub Home Page Related Content Service Related Content SR Sidebar Related Content

-

Schwoomerangs: Returning to Schwab with Nichole S. Learn why Nichole S., a Director in Talent & Organizational Development and one of our "Schwoomerangs", returned to Schwab -- and how her work helps others thrive professionally. November 14, 2023 Life at Schwab Culture & Inclusion Story Hub

-

Season of Giving: Empowering Communities Through Volunteerism with Daniel R. Daniel, United States Marine Corps Veteran and Director, is playing a crucial part in fighting food insecurity for those in need. Learn about his journey from the military to Schwab, how he's creating a positive impact through volunteerism, and the importance of lending a helping hand. November 16, 2023 Career Development Culture & Inclusion Story Hub

-

Empathy Through Art: How the “Pathos Project” Unveils Our Unique Experiences Catch up with Wannie, one of the creators of The Pathos Project, and Lindsay, a featured artists, to understand how the accessibility of art strengthens our Schwab community and unites us under common understanding. November 17, 2023 Life at Schwab Culture & Inclusion Story Hub

-

ERG Spotlight: Families at Schwab (FAMS) Learn about our Families at Schwab (FAMS) Employee Resource Group, where community, education, and networking opportunities are helping parents and guardians thrive. November 28, 2023 Life at Schwab Benefits Culture & Inclusion Story Hub

-

Schwoomerangs: Returning to Schwab with Jamie F. Read about how “Schwoomerang” Jamie, pursued career opportunities outside of our company and later returned. As a Manager in Talent Acquisition, she’s using her skills to attract top-tier talent and is happy to be with a company that prioritizes her professional growth. November 28, 2023 Benefits Career Development Culture & Inclusion Story Hub

-

Culture at Schwab: Creating Positivity with Chris W. Read how Specialist Chris W. spreads positivity and inspiration every day at Schwab. December 21, 2023 Life at Schwab Career Development Culture & Inclusion Story Hub

-

Schwoomerangs: Returning to Schwab with Maressa M. Read how Maressa M., a Manager in Event & Production Services, rediscovered our warm culture and career opportunities after returning to our team. January 04, 2024 Career Development Culture & Inclusion Story Hub

-

A Journey of Ambition and Growth: 40 Years in Financial Services Read about Wanda's professional growth, desire to help others, and impactful career spanning 40 years at Schwab. January 31, 2024 Career Development Culture & Inclusion Story Hub Home Page Related Content

-

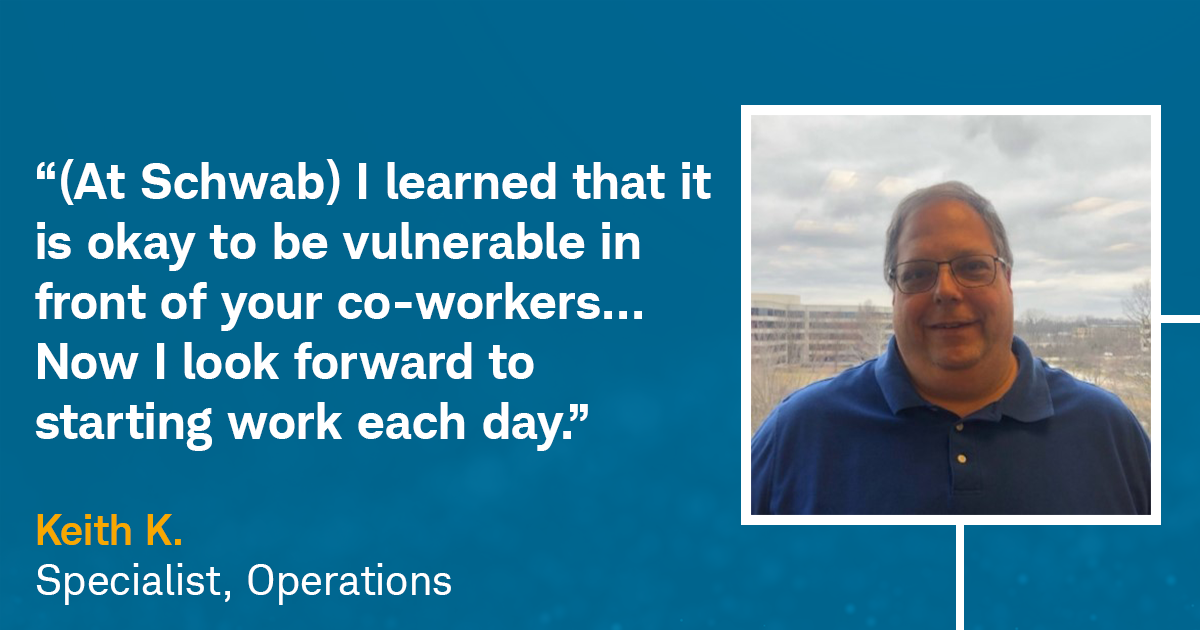

How Vulnerability Leads to Better Client Service Read how career changer Keith K. uses his empathy to serve clients - and how our caring culture empowered him to overcome obstacles, be his authentic self, and grow in his career. February 14, 2024 Career Development Culture & Inclusion Story Hub

-

25 for 25: A Wellness Challenge | Schwab Jobs Charles Schwab Abilities Network (CSAN) and Military Veteran Network (MVN), two of our 11 Employee Resource Groups at Schwab, jointly presented a mindful challenge to Schwabbies entitled the 25 for 25 Challenge. Read on to find out the significance behind the number "25" and why this challenge was so impactful! June 21, 2023 Culture & Inclusion Story Hub

-

NERDing Out: Schwab’s Associate Software Engineering Program What do you get when you combine on-the-job training, continuous learning & development opportunities, and the power to grow your skills & acumen in the tech space? You guessed it – the Associate Software Engineering program! Read on to learn why being a NERD is such a great experience for graduates in the tech space. June 21, 2023 Interns & Early Careers Story Hub

-

How to Start Networking & Make Connections Read on for networking advice from a Schwab Sourcing advisor on why it’s important and how to make meaningful connections that will help you find job opportunities and advance your career! June 21, 2023 Career Development Story Hub

-

Careers in Tech: Personalized Investing Engineering Read how Motif & Schwab combined forces to disrupt the finance industry with innovative technology and personalized investing engineering. June 21, 2023 Life at Schwab Story Hub Technology Related Content

-

Service at Schwab: Finding Fulfillment in Your Career Through Serving Clients Are you someone who genuinely enjoys helping others? Do you value improving yourself professionally and the opportunity to grow your skills all while receiving support from leadership? If this resonates with you, a career in Service may be the perfect place to start your career journey! June 21, 2023 Life at Schwab Story Hub

-

Dorian’s Journey from an HBCU to Charles Schwab | Schwab Jobs Explore what it's like to transition from college to corporate America - Learn about Dorian's journey from a Historically Black College & University (HBCU) to the finance world with Schwab. June 21, 2023 Life at Schwab Story Hub

-

Supporting First-Gen College Students: Rene's Story Schwab helps first generation college students like Rene become a Financial Consultant with employee resource groups, higher education and tuition reimbursement. June 21, 2023 Interns & Early Careers Story Hub

-

How to Turn Your Internship Into a Full-Time Career Learn tips on how to put yourself in the best position for successfully receiving a full-time job offer from your internship. June 21, 2023 Life at Schwab Story Hub

-

Intern to Financial Consultant: Catherine & Isabel’s Journey Through the FCDA Program The Financial Consultant Development Academy at TD Ameritrade is an opportunity for college graduates to make a difference in the lives of clients by helping them achieve their financial goals. Read the article to learn more about how you can make an impact in your financial services career! June 21, 2023 Interns & Early Careers Story Hub

-

Schwab's Intern Alumni: From Intern to Talent Acquisition Manager Learn how this Schwabbie turned her internship and passion for human resources into a full-time Talent Acquisition Management role. June 21, 2023 Life at Schwab Story Hub

-

An Empathetic Approach to Finance Learn how our Client Relationship Specialists help clients with their personal financial goals including wills, trusts, and estate plans all while taking an empathetic approach to finance. June 21, 2023 Life at Schwab Story Hub

-

Schwab’s Intern Alumni: From Intern to Product Manager Learn how this Schwabbie turned an internship into a full-time Product Management role while learning data analytics programs such as SQL, Python, and Tableau. June 21, 2023 Interns & Early Careers Story Hub

-

Systems Engineer and Paralympian Tony V.'s Journey Learn how Sr. Systems Engineer and former Paralympic Gold Medalist Tony V. found a support at Schwab. June 21, 2023 Life at Schwab Story Hub

-

What It’s Like Being a Software Developer Engineer | Schwab Jobs From HBCU to Schwab Technology: Amari’s Career as a Software Developer Engineer. Read about Amari's journey from his college campus to working in financial technology at Schwab! June 21, 2023 Life at Schwab Story Hub

-

Women in Tech: An Interview With Kristin, Director of Schwab's NERD Program Learn more about Schwab's NERD program and Kristin's career journey in technology. June 21, 2023 Culture & Inclusion Story Hub

-

How to Advocate for Women's Rights in the Workplace Find out how Schwab strives to be one of the best workplaces for women in business & finance through promoting gender equality & women's rights. June 21, 2023 Culture & Inclusion Story Hub

-

Celebrating Over 20 Years at Schwab: Tim’s Commitment to Service As the end of April is approaching, so is Tim R.’s length of service at Schwab. From his time in the military to his tenure at Schwab, Tim’s commitment to his clients is a great reminder of the foundation that Schwab was built on – service is at the heart of everything we do. June 21, 2023 Life at Schwab Story Hub

-

ERG Overview: How GLOBE Fosters Belonging Learn more about Schwab's employee resource group, GLOBE, and how Schwab celebrates cultural differences. June 21, 2023 Culture & Inclusion Story Hub

-

Our Culture of Appreciation We appreciate our Schwabbies each and every day! Read how appreciation is part of Schwab's culture. June 21, 2023 Culture & Inclusion Story Hub

-

How Schwab & TD Ameritrade are Integrating Their Cultures in a Virtual World Learn more about the ways in which Schwab and TD Ameritrade are joining cultures through a Culture Club that explores making connections, employee experience themes, sharing ideas, and empowering our employees to grow together. June 21, 2023 Life at Schwab Story Hub

-

Disability Advocacy in the Workplace: Schwab's Partnership with Inclusively Learn more about Schwab's partnership with Inclusively in an interview with Walt D., III. June 21, 2023 Culture & Inclusion Story Hub

-

Latinas in Tech: Overcoming Imposter Syndrome Read Jessica's story on her career progression in tech as a Latina. Find out how to build confidence, gain tech experience, & overcome imposter syndrome! June 21, 2023 Culture & Inclusion Story Hub Technology Related Content

-

Mental Health at Work: Creating Community & Navigating Neurodiversity in the Workplace As a continuation in a series around balancing mental health in the workplace, read on to learn more about Sean C.'s journey of being diagnosed with ADHD and how that has enlightened, enhanced, and altered his life, both personally and professionally. June 21, 2023 Culture & Inclusion Story Hub

-

Military Spouse Appreciation Day: An Interview with Lauren Military spouses play an important role in the military community. Read how Lauren unleashed her career at Schwab and supported her family while her husband was in the Navy. June 21, 2023 Culture & Inclusion Story Hub

-

We're Better Together: Schwab's Commitment to Giving Back | Schwab Jobs Service is at the heart of Schwab’s culture. Whether it’s serving our own Schwabbies, clients, or the communities around us, we value the opportunity to give back to those we care about. Hear from our Outstanding Community Service Award winners on how they used their Time to Volunteer benefit! June 21, 2023 Culture & Inclusion Story Hub

-

Supporting Military Veterans at Schwab: Robert W.’s Passion for Community & Engagement As a part of National Military Appreciation Month, and as a continuation in our series on balancing mental health in the workplace, Robert W. shares the impact Military Veterans Network has made on his career, how Schwab supports veterans, and the invaluable sense of community & family the ERG gives to its members. June 21, 2023 Culture & Inclusion Story Hub

-

Unleash the possibilities: Women in Tech at Schwab As Schwab continues to grow as a firm, so does our technology space. We sat down with two amazing women in tech, to ask how they’ve seen this industry grow at Schwab and what's their favorite part about being a Schwabbie! June 21, 2023 Culture & Inclusion Story Hub Technology Related Content

-

Women in Tech: Mentorship & Advocacy in Security Learn how Falycia, a U.S. Marine and technology enthusiast, got her start in security at Schwab. June 21, 2023 Culture & Inclusion Story Hub

-

Our List of the Best Schwab Blogs Highlighting the best Schwab stories on employee resource groups, benefits, early talent programs, & more. Find out our most popular Schwab blogs! June 21, 2023 Life at Schwab Story Hub

-

Career Changers: Mother and Daughter Financial Services Duo | Schwab Jobs Cindy and Randi M. made a career switch to financial services, becoming a mother & daughter duo at Schwab. June 21, 2023

-

A Culture of Service: Going Above and Beyond with Matt L. | Schwab Jobs Our Client Service & Support professionals enact positive change in the lives of our clients each and every day. For Matt L., it was only 4 months in his new position at Schwab that he was able to reflect on what bringing this purpose to life meant. Read on to find out how Matt helps his clients Own Their Tomorrow! June 21, 2023

-

Pursuing the American Dream | Schwab Jobs Read how Gio went from Bolivia to the United States and worked her way up from an entry level job to management in Financial Services at Schwab's Westlake campus. June 21, 2023 Career Development Story Hub

-

Finding Your Why: Hanna W., Brokerage Service Representative Read about Hanna W.'s journey to obtaining her Series 7 and becoming a Brokerage Service Representative June 21, 2023 Service Related Content

-

How to Advance your Career at Schwab: Exploring Alex’s Journey Education reimbursement is a benefit offered by Schwab, which aims to provide Schwabbies with opportunities to develop their skills and advance in their career. For Schwabbie, Alex B., the education reimbursement benefit helped him reach his goal of becoming a Chartered Financial Analyst! June 21, 2023 Benefits Story Hub

-

How to Advance Your Career at Schwab: Exploring Monica’s Journey in Pursuing her MBA Among Schwab’s many core values and beliefs, the desire to further one’s self in their career and ignite their passion is one that many Schwabbies have in common. Read on to find out how Monica L. advanced her career at Schwab using the tuition reimbursement benefit to earn her Masters of Business Administration! June 21, 2023 Benefits Story Hub

-

How to Prevent Burn-out: 7 Tips for Work and Home As a firm that supports work-life balance and the overall health of our employees, we’d like to provide some tips and advice that can help reduce the feeling of burn-out and get you back to a place where you feel energized and productive at work! June 21, 2023 Career Development Story Hub

-

A Financial Service Professional's Passion for Community, Teaching, & Service Kayla R. is currently a Financial Service Representative helping clients reach their financial goals. Learn how she is paving the way for others with her passion for customer service! June 21, 2023 Career Development Story Hub Service Related Content

-

How Schwab is Investing in Early Talent | Schwab Jobs Learn about how Charles Schwab is investing in the growth and opportunity of early talent. June 21, 2023

-

Kat T.: Neurodiverse Employee Empowerment | Schwab Jobs Learn how Neurodiversity at Work program hire Kat T. feels empowered to thrive at Schwab. June 21, 2023

-

Empowering Success: Finding the Support to Pass Series 7 at Charles Schwab | Schwab Jobs Learn how Schwab supported Jessica M. on her journey to passing her Series 7 exam and becoming a full-time Schwabbie. June 21, 2023 Career Development Story Hub

-

ERG Spotlight: Black Professionals at Charles Schwab | Schwab Jobs Learn how BPACS (Black Professionals at Charles Schwab) strives to advocate, educate, and celebrate the Black community. June 21, 2023

-

Career Spotlight: Reentering the Workforce with Donna M. Learn how Donna M., a Director in Trading Education, built a successful career at Schwab after being a stay-at-home mom for 11 years. June 21, 2023

-

Time Flies When You’re Having Fun: Schwabbie Sabbatical Stories For every 5 years of employment at Schwab, our employees earn a sabbatical benefit. Read what 3 Schwabbies did during their prolonged vacations. June 21, 2023 Benefits Story Hub

-

Taking a Leap of Faith: Katerina’s Story of Resilience and New Beginnings in America We believe in the power of Owning Your Tomorrow. For Katerina, owning her tomorrow included following her grandfather’s footsteps in emigrating to the U.S. and leaving the life she knew behind to create an entirely new one in America. Read on to find out more about Katerina's journey and her career at Schwab! June 21, 2023 Career Development Story Hub

-

How Employee Resource Groups Support Diversity | Schwab Jobs Learn how Geraldine uses Schwab's Employee Resource Groups (ERGs) to find diversity & inclusion, engagement, role models, and development opportunities. June 21, 2023

-

Schwab ERGs: How WINS Empowers Women in Finance | SchwabJobs Read how WINS National Co-Chair Karen B. works to build a space for women in finance that fosters career development, networking, and a sense of community at Charles Schwab. June 21, 2023

-

A Culture of Support: Caryn V.'s Journey to Recovery Learn how Caryn V. was supported by Schwabbies while recovering from a serious injury June 21, 2023

-

Find Your Fit: 10 Essential Questions to Ask During Your Job Interview To help you along your job hunting journey, we put together “10 Essential Questions to Ask During Your Job Interview”. Read through to learn how to uncover key elements of company’s culture and see how our own Schwab Talent Advisors answer these important questions. February 21, 2024 Career Development Culture & Inclusion Story Hub Home Page Related Content SR Sidebar Related Content

-

How Our WINS Allyship Program Creates Connections Allyship is a big part of how we support one another! Our WINS (Women's Interactive Network at Schwab) Allyship program connects women members to male allies, giving them the chance to bond, grow their knowledge, and build lasting relationships. Read Jessica C. and Ty G.’s experiences with the program, and how allyship continues to empower other Schwabbies to thrive! March 06, 2024 Career Development Culture & Inclusion Story Hub

-

January 18, 2024

-

A Sabbatical Journey: An Analytics Consultant’s Exploration of Europe and Work-Life Balance at Schwab. Learn how a data analytics consultant utilized his Schwab sabbatical benefit to backpack Europe and enjoy some work-life balance. March 19, 2024 Benefits Story Hub Home Page Related Content SR Sidebar Related Content

-

Having Fun and Transforming Lives: Tiara Thursday Read how our Omaha Advisor Services Estates team created “Tiara Thursday,” a creative way to bond, laugh, and symbolize their commitment to enjoying the important work they do. March 25, 2024 Life at Schwab Culture & Inclusion Story Hub

-

GLOBE: A place to belong and understand other cultures It’s Celebrate Diversity Month, a time where we highlight the cultures that make up our community at Schwab. Learn how our GLOBE Employee Resource Group brings many different cultures together to create shared understanding and celebrate our differences. April 03, 2024 Culture & Inclusion

-

Prioritizing Career Development with Pro Day To support the development of our people, we got together to dive deep into areas we're passionate about, giving us time to hone our skills and explore new avenues for growth in our roles and careers. Read about how we used Pro Day to elevate ourselves and each other! April 17, 2024 Career Development Story Hub Home Page Related Content SR Sidebar Related Content

-

Connecting Cultures and Fostering Inclusion at Schwab May is Asian American Native Hawaiian Pacific Islander Heritage Month! Across the country, chapters of the Asian Professionals Inclusion Network at Schwab (APINS) host celebratory and educational events all year long. Their efforts, along with learning about the experiences of Schwabbies like Mary, help us foster an inclusive company culture and better serve our communities. May 08, 2024 Culture & Inclusion Story Hub

-

Schwoomerangs: Employees Who Return to Schwab with Harvey L. Meet Harvey L., a Director of Business Strategy in Wealth and Advice Solutions, who briefly left and then came back to Schwab – and rediscovered our warm culture and career advancement opportunities. May 10, 2024 Career Development Culture & Inclusion Story Hub

-

May 20, 2024

-

May 20, 2024

-

How Former Army Reservist Jack B. Continues to Serve Jack B.'s commitment to helping others shines through in everything he does. Read about his journey from the military to our company, his dedication to volunteerism, and how he makes a difference both in and out of the office! May 10, 2024 Career Development Culture & Inclusion Story Hub

-

Creating Juneteenth Traditions with Jannibah C. Juneteenth is an important day of celebration and reflection. To learn more about what this day means to our peers, we met with Jannibah C., a Director in Communications. Read her thoughts about the holiday, how it creates togetherness for the Black community, and more. June 10, 2024 Life at Schwab Culture & Inclusion Story Hub

-

Career Tips: How to Start Building Your Professional Network Learn essential career tips to start building your professional network. Discover effective networking strategies and best practices for in-person and virtual connections. Boost your career today! June 27, 2024 Career Development Story Hub

-

ERG Spotlight: Charles Schwab Abilities Network Learn about our Charles Schwab Abilities Network (CSAN) Employee Resource Group (ERG), which strives to foster a supportive work environment and community for those who have, or care for a loved one with, a disability. June 28, 2024 Life at Schwab Culture & Inclusion Story Hub

-

April 29, 2024

-

June 07, 2024

-

Career Spotlight: Dani N.'s Career Development Journey | Schwab Jobs Learn how Dani used Schwab's professional development opportunities to advance in her career. June 21, 2023

-

Richard's Journey: The Power of Financial Literacy Learn how Richard discovered the power of financial literacy through mentorship, training, and by joining Schwab's Financial Consultant Academy. June 21, 2023 Career Development Story Hub Retail Related Content

-

Rhiannon's Journey to a Career in Financial Services | Schwab Jobs Have you ever transitioned from one industry to another in your career journey? For Rhiannon C., she took her degree in political science and landed a job in Service at TD Ameritrade. Find out how her passion for helping others led her to a career in Financial Services! June 21, 2023 Career Development Story Hub

-

New Year, New Career? Tips to Improve Your Career Path | Schwab Jobs Whether you’re trying to increase your pay, find new opportunities, develop your current career path, or just find something different – these tips will help you achieve your goals. June 21, 2023 Career Development Story Hub

-

Career Spotlight: Navit J. on Mentorship and Career Growth | Schwab Jobs Learn How Navit J., a Managing Director in Corporate Compliance, used mentorship to grow her career. June 21, 2023

-

Lea's Path to Leadership in Financial Services & Tech Learn how Lea S. built an impactful career as a woman in the digital space at Schwab. June 21, 2023 Career Development Story Hub

-

Build a Career at Schwab: Hear Randy's Story Randy started off as an intern in Schwab's Intern Academy. Little did he know, his career path would twist and turn as he progressed his career as a full-time Schwabbie. June 21, 2023 Career Development Story Hub Service Related Content

-

Build a Career at Schwab: Hear Taji's Story | Schwab Jobs Taji started off as an intern at Schwab and since then, has advanced from an entry-level position to the current role she is in today. Read on to find out more about her experience moving up in the company! June 21, 2023 Career Development Story Hub

-

Build a Career at Schwab: Hear Matthew's Story | Schwab Jobs They say time flies when you're having fun! For Schwabbie Matthew B., it's been 5 years since his start as an intern back in 2014. Read on to find out how Matthew's exciting career journey started in the hospitality industry and ended up in a software engineering role! June 21, 2023 Career Development Story Hub

-

AAPI Heritage and Inclusion with Michelle and Yang | Schwab Jobs APINS ERG co-chairs discuss celebrating AAPI Heritage Month and empowering AAPI voices in finance. June 21, 2023

-

ERG Spotlight: Asian Professionals Inclusion Network APINS | Schwab Jobs Read how the APINS community uses members' diverse experiences to promote awareness and inclusion. June 21, 2023

-

From Law Enforcement to Financial Services: Stacie Shares Her Career Journey At Schwab, we welcome individuals from all different backgrounds and career fields. For Stacie, her career journey as a Law Enforcement officer ultimately led her to her current role in financial services. June 21, 2023 Career Development Story Hub

-

Teacher Builds New Career in Data Analytics Learn how Rebecca, a former math teacher, found career growth and new opportunities within Charles Schwab's Data Analytics and Insights team. June 21, 2023 Career Development Story Hub

-

Career Changer Leads to Long Term Success at Schwab Many Schwabbies come from different backgrounds and prior career fields. For Kris A, this current Schwabbie made a full 360 with starting off in the finance industry, to becoming a personal property appraiser, and then returning back to finance with Schwab. Read more about her journey below! June 21, 2023 Career Development Story Hub

-

Jannibah's Schwab Story Jannibah was on the hunt for a new career and with a background in non-profit and communications, a job in finance never crossed her mind. Learn how she came to find Schwab and why a career in financial services was the right choice for her! June 21, 2023 Career Development Story Hub

-

Katie's Schwab Story Katie's journey to Schwab started from her background in the non-profit space. As she earned her Ph.D., she soon realized that becoming a university professor wasn't for her. Instead, Katie took her passion for improving workplace culture to a new role at Schwab, which aligned with her personal values. June 21, 2023 Career Development Story Hub

-

How to Have a Successful Job Hunt as a Veteran: 5 Tips from a Schwab Recruiter Transitioning from the military to civilian life can be difficult. For those Veterans who are looking at their next career opportunity at Schwab or beyond, this article can help with how to best prepare for your new career! Read on to find how you can have a successful job hunt as a Veteran. June 21, 2023 Career Development Story Hub

-

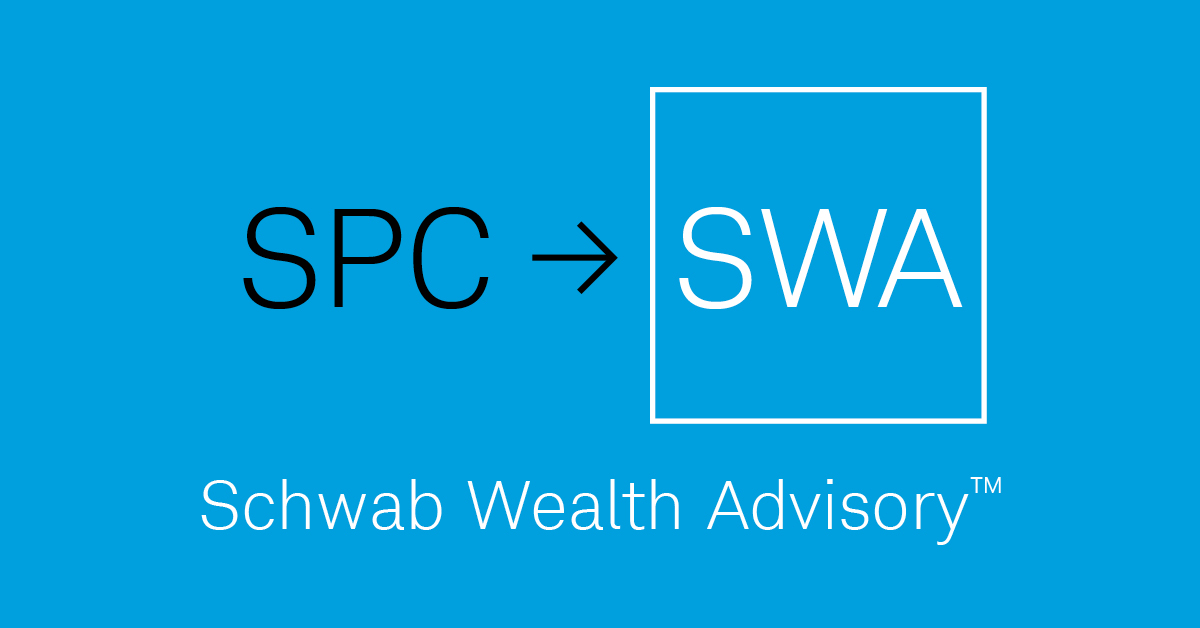

Schwab Wealth Advisory: Wealth Advisor Career Opportunities Explore how the Schwab Wealth Advisory™ name change provides opportunities for financial service professionals and advisors looking to ignite their career. June 21, 2023 Career Development Story Hub

-

ERG Spotlight: Women’s Interactive Network WINS | Schwab Jobs Learn how our WINS employee resource group supports gender equality, diversity & inclusion, and women in finance through workshops, community outreach, and more. June 21, 2023

-

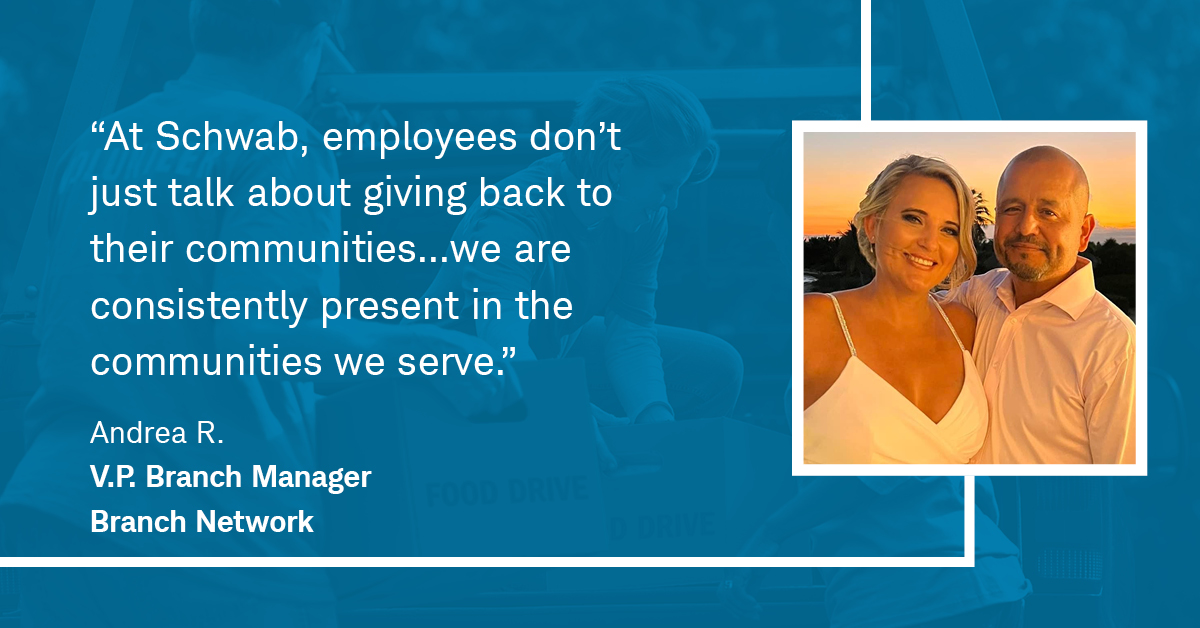

Culture of Service: Andrea R.'s Volunteering Experience | Schwab Jobs Learn how Andrea R., a V.P. Branch Manager, paired with Schwab to serve her community June 21, 2023

-

Juneteenth CeLiberation Learn about Black Professionals at Charles Schwab (BPACS) Employee Resource Group and how they are celebrating with events that promote togetherness through camaraderie, food, dance, fun and education. June 19, 2023 Culture & Inclusion

You have no recently viewed jobs

You have no saved jobs

Share: